![Responsible investing]()

by Jo Cheramie | 30 Jul, 2020 | Investment

What is responsible investing?

What is responsible investing and is it just another piece of jargon that is difficult to understand and bears no relation to our day to day life? At Christian KiwiSaver Scheme, we believe that responsible investing is an important foundation for choosing the investments that we undertake on behalf of our members.

Looking at it straightforwardly, responsible investing could be compared to shopping for eggs in the supermarket. When you find the eggs on the supermarket shelves, you are confronted by a range of different choices – bio organic eggs, paddock eggs, free-range, caged, cage-free, barn raised, etc. The selection is vast and comes with a range of prices to match your choice. So how do you choose? Would you buy solely on the price going for the cheapest eggs no matter what? Would you prefer organic eggs? Or perhaps you are concerned for the chicken’s welfare and would not select eggs from caged chickens?

On a personal level in the egg scenario, if animal welfare is an ethical concern for you and you respond by choosing free-range eggs, you could be considered to be behaving like a responsible investor.

On a broader level, when you (or your KiwiSaver provider on your behalf) are investing responsibly, you are considering investments which reflect your values and take into account how companies manage their responsibilities, for example in their dealings with the environment or the community.

You may recall either working for or hearing about, companies that were out to maximise their profit no matter the cost. However, over recent years, there has been a move to balance the interests of shareholders with other concerns such as social and environmental welfare.

There has been a big change in our supermarkets with plastic bags being replaced by reusable ones. There had been community concern about the effect that plastic bags were having on the environment due to the sheer numbers going into landfills and turning up in our waterways and oceans. This concern about the impact on our environment influenced the government to put laws in place to reduce the amount of plastic being used.

As a community, we have become interested in a variety of social and environmental issues, and this has translated into broader concerns about where KiwiSaver funds are invested. At Christian KiwiSaver Scheme we seek to avoid investments in products such as tobacco, guns and other arms manufacturing, gambling, and adult entertainment. How companies behave with regard to the environment, their employees and others, and the way they govern themselves are also things we think about when making investment decisions for our members.

Not already a member of Christian KiwiSaver Scheme? Join other like-minded Kiwi Christians growing their savings ethically today!

Membership of the Christian KiwiSaver Scheme is offered only to:

- employees of organisations whose primary activities are in our opinion Christian mission or ministry. This includes employees of charitable entities associated with or operating in the Christian Church, or employees of entities which we approve as having a Christian special character; and

- persons who express a Christian faith and have a commitment to Christian community involvement when applying (and their immediate family members and dependants).

Christian KiwiSaver Scheme is managed and issued by The New Zealand Anglican Church Pension Board (trading as Anglican Financial Care). The Product Disclosure Statement and Fund Updates are available under Documents.

![Responsible investing]()

by Editor | 1 May, 2020 | Investment, Reporting

What a quarter! It may be disappointing if your balance has declined with the negative investment returns, however, it should be remembered that the last quarter is just that – one quarter – and that your KiwiSaver account has benefited from an extraordinary run of positive quarters in recent years. In fact, returns for the last 12 months (and longer) across all our funds are positive. Nevertheless, it is timely to assess if your investment portfolio is aligned to your personal situation. We have a useful article on our website that may help you with this if you are unsure.

How did the markets react to Covid-19?

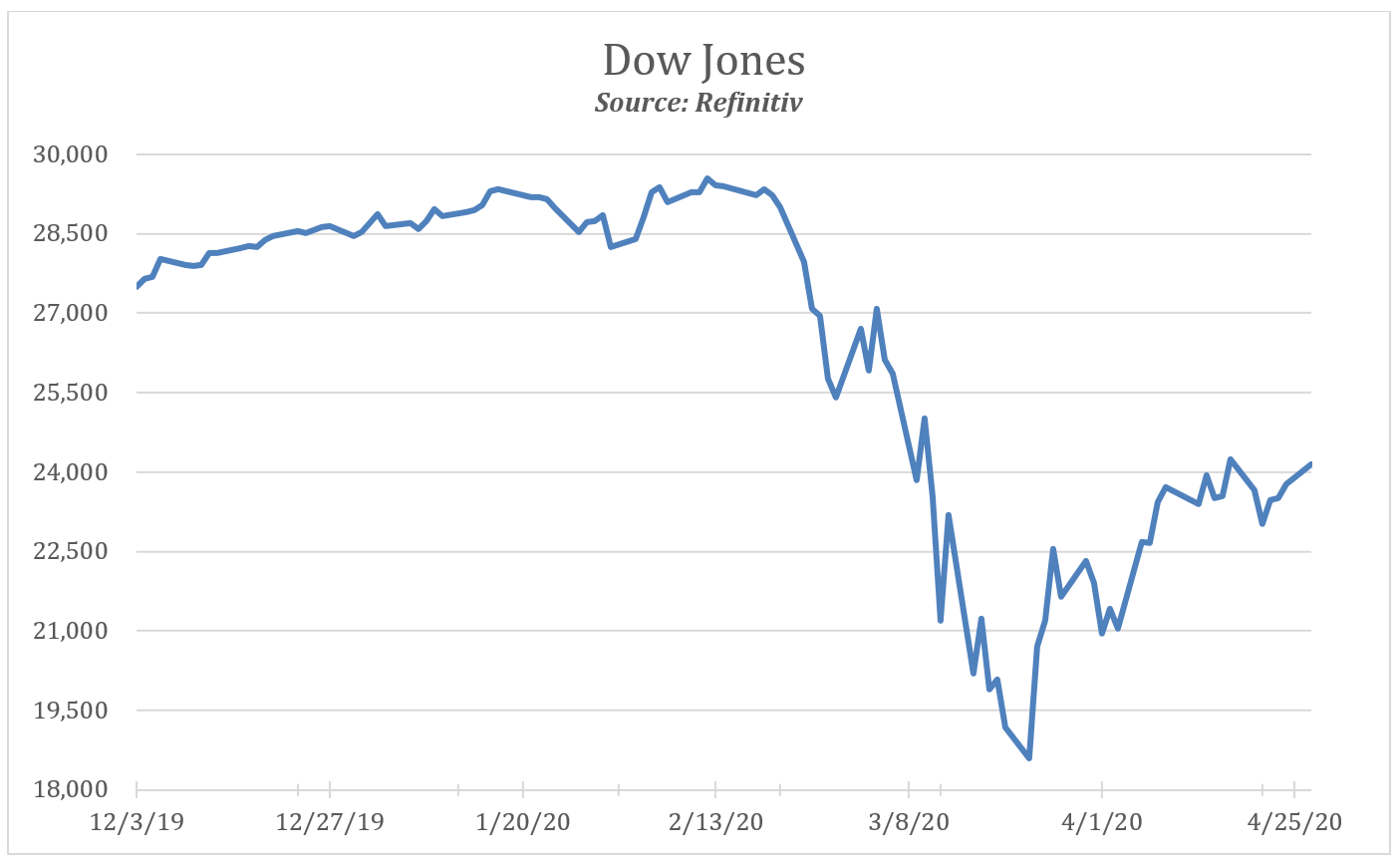

International markets were highly volatile throughout the last quarter due to the impact of Covid-19. As an indication of the large and sudden movements we saw across the last quarter, we have attached the following graph of the Dow Jones index (the commonly referred to USA equity index) which fell 27% from the end of February to late March i.e. in only about three weeks! It then rose by about 30% in the next three weeks. However, this was still about 15% below the December 2019 year-end level (The Dow Jones fell 23% in the quarter). A similar picture to the Dow Jones index has been seen across other markets around the globe.

What has the response been from Governments around the world?

We have seen a number of different responses from Governments around the world ranging from how quickly they reacted to addressing Covid-19 through to the type of level restrictions that they have adopted to fight the virus. Despite the different approaches in how they have handled lockdown restrictions, one thing that is being seen across the board is the large sums of money being spent by governments in an attempt to keep their economies turning over. This has been the case for the New Zealand Government with further announcements still expected.

When can we expect market volatility to stabilise?

Judging by the rebound in shares (at the time of writing April 2020), investors seem to think the worst has passed. It could be said lockdowns are easy to go into but very hard to come out of in terms of economic recovery. We think many uncertainties still remain and that there are probably more questions now than answers, not just with regards to the virus, but concerning the short term and longer-term economic impacts.

This health crisis is also an economic crisis. Will a successful treatment be developed, and when? How long might the lockdowns last? What steps need to be taken to get back to some normality? Will the new normal look different? How will the debt that Governments are taking on be repaid? Answers to these, and many questions, will be very relevant to investment decisions. Nevertheless, judging from history, the global economy will inevitably recover from this crisis.

We are constantly mindful of the environment in which we operate. As had been noted many times in the past within our commentaries, our investment strategy in recent times has been focused first and foremost on protecting your investment. Our experienced in-house investment team was already concerned about high share prices. Your funds will have benefited in the past quarter from this cautious approach.

You can rest assured that we are vigilantly monitoring the situation daily and managing your fund the best we can as we continue to navigate our way through these unique times.

Investment returns at 31 March 2020, before fees and tax:

The table with ID 13 not exists.

![Responsible investing]()

by Editor | 3 Feb, 2020 | Investment

The great run continued into the last quarter of 2019. The return from shares was particularly good and led to solid Growth and Balanced Fund returns (given their preference toward shares). The quarter’s returns benefitted from the reduced concerns around trade discussions between the US and China, supported by earlier reductions in interest rates and a growing view that international growth may improve.

It should be remembered that the great returns ‘last year’ are flattered somewhat given the terrible last quarter of 2018 i.e. returns in the last year benefitted from the rebound / recovery from that quarter.

Shares prices continue to rise and interest rates remain at low levels. Your funds continue to participate in these performing markets. The funds remain diversified, emphasize quality, are cautiously invested and focussed on longer term returns.

Investment returns at 31 December 2019, before fees and tax:

The table with ID 11 not exists.

![Responsible investing]()

by Editor | 3 Feb, 2020 | Investment

The question on every investors mind is – what will returns be like in the future?

As the future is unknown all that one can do is try and prepare for it. And maybe learn from the past. Throughout history investors were concerned with the ‘topic’ of the time. No doubt some ‘topics’ had a major influence on short term returns at that time.

However long term returns have almost always been good. And whilst ‘topics /events’ will always happen one needs to remember that the influence from those events will eventually pass. Exactly how much the influence will be and for how long depends on the event.

With that in mind – What is troubling investors? What are those ‘topics’ now? As always, and depending on who you talk to, the list could be long. From our perspective that list could include (and in no particular order) international trade developments, unrest in the Middle East, politics, cyber-attacks, China and climate change etc. Some of these concerns may always be on the list. Combined with what are considered elevated asset prices at the moment (both shares and bonds) we, like many others, would not be surprised if future returns (short term, and at some point) are not as high as recent gains.

One should remember that sometimes the ‘event’ could be very beneficial to returns too.

That said – What can we can we do about it? No one can predict how any of these events will impact markets in the short term however markets tend to grind higher in the long term as the economy progresses. Short-term events and market movements are outside an investors’ control.

It is more important for investors to focus on what is in their control. An appropriate savings plan is an important part of that mix. Any savings should also be diversified (across different shares and bonds, and geographically) and in quality investments (as per in all our funds).

by Editor | 3 Feb, 2020 | Investment

Managing an ethical investment portfolio requires constant care, awareness and analysis. A sector that has particular significance currently is energy. We strongly believe in a lower carbon future and that society needs to transition away from fossil fuels as quickly as possible, but reflecting this belief in our investment strategy requires a balanced and considered approach.

Our Chief Executive, Mark Wilcox, outlines our thinking around fossil fuels:

Anglican Financial Care (who manages the Christian KiwiSaver Scheme) has a policy on fossil fuels but this does not extend to full divestment.

First and foremost, we stand by biblical principles which infer creation is to be cared for and protected for future generations. In our opinion, the 2015 Paris Agreement targets infer risks to companies within the energy sector who don’t appropriately adapt their business models. We have elected to respond by excluding exposure to coal and tar sands companies and to rank other energy companies according to their extent of contribution towards a lower-carbon world.

We recognise that fossil fuel divestment is a matter of importance to the Church and that some of us share a sense of frustration with the lack of progress towards the Paris Agreement targets. However, while the future is renewables and green technology, and progress has been made, fossil fuels will still be the planet’s dominant fuel source for a long time yet (likely at least until 2050). Accordingly, there would be considerable financial risk to our members in taking a full divestment approach at this stage.

In recognition that part of the solution lies with alternative energy solutions, we have made a significant investment in a global alternative energy fund. We also have a long-standing forestry investment. We recently sold the cutting rights to the trees but has retained full ownership of the land and is currently re-planting.

For a more detailed analysis on investing towards a renewable and green technology future, we recommend a Wells Fargo white paper: It’s Not Easy Being Green—The Future of Fossil Fuels.

The bottom line is that our lives revolve around energy use, and lots of it. Fossil fuels generate most of that energy today. Recent progress in renewables and green technology has been made, and it is the future. The green movement has investors believing that fossil fuel use will soon die. We are doubtful. It takes energy to create energy, and green technologies often require fossil fuel use too. Additionally, emerging market energy use continues to climb higher. By 2050, the planet’s dominant fuel source will still likely be fossil fuels. For the planet’s sake, let’s hope that green progress has a higher gear still.

If you would like to check for yourself how Christian KiwiSaver Scheme investments mitigate the impact of climate change or to see – as ethical investors – what we do invest in, visit our website or call us on (0508) 738 473.

![Responsible investing]()

by Editor | 29 Oct, 2019 | Investment

The quarter had another positive performance with both shares and bonds (fixed interest securities) performing strongly in the quarter. Longer term returns are also positive with growth assets (with their higher weighting toward shares) outperforming the more conservative income assets (and their weighting toward bonds). The positive returns continued despite the many uncertainties in the quarter e.g. ongoing US and China trade tensions, talk of US presidential impeachment, Hong Kong riots, Brexit developments and the attack on Saudi oil production.

No doubt some of this uncertainty weighed on investor minds and led to a softening in the growth outlook. Central Banks (Government owned banks but independent) indicated further easing (i.e. lower interest rates), trying to offset the reduced growth outlook.

Despite the many uncertainties the funds continue to achieve good gains. Whilst investor sentiment could affect short term returns we continue to invest (cautiously) focussing on long term performance.

Investment returns at 30 September 2019, before fees and tax:

The table with ID 10 not exists.